But asked twice whether he would accept a budget that did not include provisions for additional tax cuts for the middle class, or that did not launch a cap-and-trade program to reduce greenhouse gas emissions, Mr. Obama demurred. Instead, he called for “a serious energy policy that frees ourselves from dependence on foreign oil and makes clean energy the profitable kind of energy” — implicitly suggesting that cap-and-trade, though he supports it, might have to wait. As for the middle-class tax cut that Mr. Obama would pay for with revenue from a cap-and-trade program, the president said, “we already had that” in the stimulus package. “We know that that’s going to be in place for at least the next two years. We had identified a specific way to pay for it. If Congress has better ideas in terms of how to pay for it, then we’re happy to listen.”

Category : President Barack Obama

A Washington Post Editorial: Softening the Wish List

Martin Feldstein: A Deduction From Charity

President Obama’s proposal to limit the tax deductibility of charitable contributions would effectively transfer more than $7 billion a year from the nation’s charitable institutions to the federal government. But the high-income taxpayers affected by the rule change are likely to cut their charitable giving by as much as the increase in their tax bills, which would, ironically, leave their remaining income and personal consumption unchanged.

In effect, the change would be a tax on the charities, reducing their receipts by a dollar for every dollar of extra revenue the government collects. It is hard to imagine a rationale for taxing schools, hospitals, medical research budgets and arts organizations in this way. I suspect that the administration officials who drafted this proposal did not understand that it would have this perverse effect.

President Points To Progress on Economic Efforts

President Obama sought to reassure Americans last night that his administration has made progress in reviving the economy and said his $3.6 trillion budget is “inseparable from this recovery.”

After sprinting through his first months in office, Obama is now facing heightened criticism from Republicans, who have called his blueprint irresponsible, and from skeptical Democrats who have already set about trimming back his top budget priorities.

Obama came into office amid lofty expectations and the worst economic crisis in generations, and he succeeded in pushing through a $787 billion stimulus and launching expensive plans to revive the banking system.

Last night, against a backdrop of a broad national anxiety that the economy may still be failing, he attempted to recalibrate the high hopes to more closely fit the challenges he said lie ahead.

Carmen Reinhart and Kenneth Rogoff: The history of banking crises indicates this one may be far from

The good news from our historical study of eight centuries of international financial crises is that, so far, they have all ended. And we confidently predict this one will end, too. We are just not quite so sure it will be nearly as soon as the chirpy forecasts coming from policymakers around the globe. The U.S. administration, for example, is now predicting that growth will renew in the latter part of this year and continue at a brisk pace of 4 percent for several years thereafter. Is this a fact-based forecast or wishful thinking?

A careful look at the international evidence on severe banking crises suggests a far more cautious assessment. The recessions that follow in the wake of big financial crises tend to last far longer than normal downturns, and to cause considerably more damage. If the United States follows the norm of recent crises, as it has until now, output may take four years to return to its pre-crisis level. Unemployment will continue to rise for three more years, reaching 11”“12 percent in 2011.

Toxic Asset Plan May Woo Investors, but Long-term Impact Is Unclear

…[DONALD MARRON] I hope the government has set it up that, once it gets going, they can change the terms, as the market gets more comfortable, as more confidence this thing is actually going to work, isn’t as concerned about what the Congress is going to do as they are in the case of TALF.

So this is getting things going. There needs to be flexibility in the future. I’m assuming Tim Geithner and Larry Summers have thought that through. So once we get it started, we can make sure it becomes a positive continuing force and not some kind of a windfall.

JEFFREY BROWN: Well, Mr. Krugman, go ahead. Argue back. That’s the argument is, you need to attract investors, so…

PAUL KRUGMAN: I don’t think that’s the issue, really. I mean, there’s a lot of people who’ve got money parked in the banks. The problem is that people — it’s the banks as institutions that are the issue, not whether people are willing to buy these particular assets.

In a way, we’d like to make the whole story of these assets go away. The only reason that they’re there, the only reason it’s an issue is because the banks have lost so much money that they are not effective at their job of passing funds from one end of the economy to the other.

This is not going to change that. I mean, it’s going to make some of the stuff sell for a slightly better price, but the banks are still going to be deep underwater, at least the troubled ones are going to be. It’s going to convey some windfall benefits to people who are holding some of this paper who are not actually crucial financial intermediaries.

Pretty Soon it Adds up to Real Money

{kind=link}

George Soros: Credit default swaps need much stricter regulation

In all the uproar over AIG, the most important lesson has been ignored. AIG failed because it sold large amounts of credit default swaps (CDS) without properly offsetting or covering their positions. What we must take away from this is that CDS are toxic instruments whose use ought to be strictly regulated: Only those who own the underlying bonds ought to be allowed to buy them. Instituting this rule would tame a destructive force and cut the price of the swaps. It would also save the U.S. Treasury a lot of money by reducing the loss on AIG’s outstanding positions without abrogating any contracts.

CDS came into existence as a way of providing insurance on bonds against default. Since they are tradable instruments, they became bear-market warrants for speculating on deteriorating conditions in a company or country. What makes them toxic is that such speculation can be self-validating.

Up until the crash of 2008, the prevailing view — called the efficient market hypothesis — was that the prices of financial instruments accurately reflect all the available information (i.e. the underlying reality). But this is not true. Financial markets don’t deal with the current reality, but with the future — a matter of anticipation, not knowledge. Thus, we must understand financial markets through a new paradigm which recognizes that they always provide a biased view of the future, and that the distortion of prices in financial markets may affect the underlying reality that those prices are supposed to reflect.

U.S. Seeks Expanded Power to Seize Firms

The Obama administration is considering asking Congress to give the Treasury secretary unprecedented powers to initiate the seizure of non-bank financial companies, such as large insurers, investment firms and hedge funds, whose collapse would damage the broader economy, according to an administration document.

The government at present has the authority to seize only banks.

Irwin Stelzer: Soon there may be nobody left to lend to America

Meanwhile, there is little prospect that Congress will do what is necessary to bring spending and borrowing down to levels that do not trigger inflation. Politicians just don’t worry as much about inflation as about catering to their multiple constituencies. So the Treasury will have more trillions in IOUs to peddle.

But its best customers just might be unenthusiastic about adding significantly to their holdings. Wen already owns trillions in Treasury bills that are depreciating in value. Besides, China’s mounting needs for infrastructure and an improved safety net will sop up funds once used to buy American securities. Japan, another large customer, is now running a current-account deficit, and so it won’t have as many dollars to recycle. Nor will Middle East buyers, no longer receiving a flood of dollars from $140-a-barrel oil. Little wonder that Larry Lindsey, former economic adviser to President George W Bush, says he “cannot figure out what combination of foreign buyers is going to acquire . . . [the] debt” that Obama’s plans will generate.

Which leaves Americans and the Fed as customers. Even if they save more, domestic consumers can’t absorb all the Treasury bonds that will be on offer. And if the Fed keeps buying, it will pour fuel on the inflationary fires.

RNS: Will Obama tax plan hurt religious groups?

President Obama’s proposed 2010 federal budget contains a 7% cut in charitable tax deductions for the nation’s wealthiest taxpayers. Some religious groups are asking how that will affect their bottom line.

The answer: it depends who you ask.

Here’s what it means in real terms for the 5% of Americans whose household income exceeds $250,000 a year. Those families can currently save $350 in taxes for every $1,000 donated to charity; under Obama’s plan, that amount would drop to $280 per $1,000 donation.

“By doing this, you raise the cost of giving” said Roberton Williams, a senior fellow at The Tax Policy Center, a liberal Washington think tank.

Brad Delong: The Geithner Plan FAQ

Q: What is the Geithner Plan?

A: The Geithner Plan is a trillion-dollar operation by which the U.S. acts as the world’s largest hedge fund investor, committing its money to funds to buy up risky and distressed but probably fundamentally undervalued assets and, as patient capital, holding them either until maturity or until markets recover so that risk discounts are normal and it can sell them off–in either case at an immense profit.

Q: What if markets never recover, the assets are not fundamentally undervalued, and even when held to maturity the government doesn’t make back its money?

A: Then we have worse things to worry about than government losses on TARP-program money–for we are then in a world in which the only things that have value are bottled water, sewing needles, and ammunition.

Q: Where does the trillion dollars come from?

A: $150 billion comes from the TARP in the form of equity, $820 billion from the FDIC in the form of debt, and $30 billion from the hedge fund and pension fund managers who will be hired to make the investments and run the program’s operations.

Q: Why is the government making hedge and pension fund managers kick in $30 billion?

A: So that they have skin in the game, and so do not take excessive risks with the taxpayers’ money because their own money is on the line as well.

Read it all–and the discussion.

Update:: Paul Krugman doesn’t like the plan.

Timothy Geithner: My Plan for Bad Bank Assets

The Public-Private Investment Program will purchase real-estate related loans from banks and securities from the broader markets. Banks will have the ability to sell pools of loans to dedicated funds, and investors will compete to have the ability to participate in those funds and take advantage of the financing provided by the government.

The funds established under this program will have three essential design features. First, they will use government resources in the form of capital from the Treasury, and financing from the FDIC and Federal Reserve, to mobilize capital from private investors. Second, the Public-Private Investment Program will ensure that private-sector participants share the risks alongside the taxpayer, and that the taxpayer shares in the profits from these investments. These funds will be open to investors of all types, such as pension funds, so that a broad range of Americans can participate.

Third, private-sector purchasers will establish the value of the loans and securities purchased under the program, which will protect the government from overpaying for these assets.

Politico on Obama's 60 minutes Interview

The interview captured the balancing act that Obama must strike on the economy. He gave a nod to public anger at Wall Street while saying it could not dictate his response.

He got in a few whacks of his own at Wall Street executives who contributed to the meltdown””referring to them ironically at one point as “the best and the brightest”””while being ever-mindful that he still needs their help to dig out of the crisis.

His talk of depression could be viewed as alarmist””but it also seemed aimed at bracing Congress and the public for the unpopular prospect of spending even more taxpayer dollars to prop up Wall Street. Treasury Secretary Timothy Geithner is set to roll out a plan Monday aimed at restoring the flow of credit that would back up private investments with government funds.

Even his awkward laughter highlighted an issue Obama has faced dating back to the campaign, a sense that he sometimes is too “cool” and detached to fully grasp the public anxiety over mounting job losses and economic worries.

Governor Mark Sanford: Why South Carolina Doesn't Want 'Stimulus'

America’s states are laboratories of democracy. They are both affected by, and relevant to, the larger national debate. What we’ve found in our own corner of the country is that carrying a substantial debt load limits our options when it comes to running government.

A recent report by the American Legislative Exchange Council ranked us 47th worst in the nation for annual debt service as a percentage of tax revenue. Our state dedicates nearly 11% of its annual tax revenue to paying debt. On top of that, South Carolina has another $20 billion in unfunded, long-term political promises for pensions and other liabilities. The state budget has already been cut four times in recent months as the national economic downturn has impacted South Carolina and driven down tax revenue.

Banker fury over tax ”˜witch-hunt’

Bankers on Wall Street and in Europe have struck back against moves by US lawmakers to slap punitive taxes on bonuses paid to high earners at bailed-out institutions.

Senior executives on both sides of the Atlantic on Friday warned of an exodus of talent from some of the biggest names in US finance, saying the “anti-American” measures smacked of “a McCarthy witch-hunt” that would send the country “back to the stone age”.

There were fears that the backlash triggered by AIG’s payment of $165m in bonuses to executives responsible for losses that forced a $170bn taxpayer-funded rescue would have devastating consequences for the largest banks.

“Finance is one of America’s great industries, and they’re destroying it,” said one banker at a firm that has accepted public money. “This happened out of haste and anger over AIG, but we’re not like AIG.”

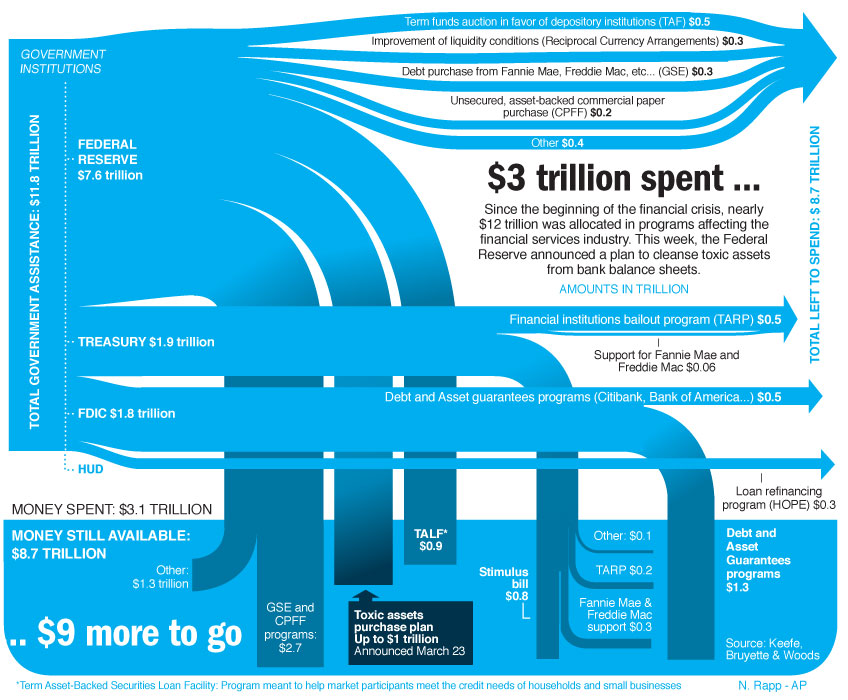

AP: Treasury's toxic asset plan could cost $1 trillion

The Obama administration’s latest attempt to tackle the banking crisis and get loans flowing to families and businesses rely on a new government entity, the Public Investment Corp. to help purchase as much as $1 trillion in toxic assets on banks’ books.

The plan that Treasury Secretary Timothy Geithner intends to announce Monday aims to use the resources of the $700 billion bank bailout fund, the Federal Reserve and the Federal Deposit Insurance Corp.

Thomas Friedman: Are We Home Alone?

I ran into an Indian businessman friend last week and he said something to me that really struck a chord: “This is the first time I’ve ever visited the United States when I feel like you’re acting like an immature democracy.”

You know what he meant: We’re in a once-a-century financial crisis, and yet we’ve actually descended into politics worse than usual. There don’t seem to be any adults at the top ”” nobody acting larger than the moment, nobody being impelled by anything deeper than the last news cycle. Instead, Congress is slapping together punitive tax laws overnight like some Banana Republic, our president is getting in trouble cracking jokes on Jay Leno comparing his bowling skills to a Special Olympian, and the opposition party is behaving as if its only priority is to deflate President Obama’s popularity.

I saw Eric Cantor, a Republican House leader, on CNBC the other day, and the entire interview consisted of him trying to exploit the A.I.G. situation for partisan gain without one constructive thought. I just kept staring at him and thinking: “Do you not have kids? Do you not have a pension that you’re worried about? Do you live in some gated community where all the banks will be O.K., even if our biggest banks go under? Do you think your party automatically wins if the country loses? What are you thinking?”

Obama Seeks to Increase Oversight of Executive Pay

The Obama administration will call for increased oversight of executive pay at all banks, Wall Street firms and possibly other companies as part of a sweeping plan to overhaul financial regulation, government officials said.

The outlines of the plan are expected to be unveiled this week in preparation for President Obama’s first foreign summit meeting in early April.

Increasing oversight of executive pay has been under consideration for some time, but the decision was made in recent days as public fury over bonuses has spilled into the regulatory effort.

An LA Times Editorial: Wise up, Mr. Geithner

When President-elect Barack Obama picked Timothy F. Geithner to be his Treasury secretary four months ago, numerous analysts praised the choice because of Geithner’s expertise in the financial industry. He was president of the Federal Reserve Bank of New York at the time, and had helped craft the response to the troubles roiling global credit markets. But as the debacle over the American International Group bonuses has made clear, Geithner’s knowledge about Wall Street is matched by his ignorance about the political culture of Washington. And the blunders committed by Geithner (and others, including the Federal Reserve and previous Treasury Secretary Henry M. Paulson) could undermine key elements of President Obama’s economic recovery plan.

Terence Corcoran: Is this the end of America?

But America is at risk in other ways, especially in the technical business of setting and executing policy. The presidency of Barack Obama has set out on a course that has no precedent in U.S. history. Franklin D. Roosevelt, whose New Deal transformed the U.S. economy during the Great Depression, pushed America off on a sharply different political and ideological course. The Obama administration is different in many ways, not least in its supreme self-confidence in its methods and objectives.

Reform of health care, environmental policy, education, energy, banking, regulation ”” every nook and cranny of the U.S. economy has been put on alert for major change. Expansion of government spending, plunging the U.S. into unprecedented deficits, is without parallel. In economic policy, through regulation and control of energy output, financial services and monetary expansion, the U.S. government has embarked on a fundamental reshaping of America. It is designed, in short, to bring on the end of America.

The spillover effect of all this on the rest of the world promises to be dramatically disruptive. The greatest global risk is in monetary and currency policy. Below is a chart that graphically demonstrates the sharp deviation in monetary policy from past norms. Under the chairmanship of Ben Bernanke, the Federal Reserve is in the midst of a giant economic experiment, flooding the world with U.S. dollars, hoping that flood will stimulate economic activity.

David Brooks: Perverse Cosmic Myopia

In times like these, you’d expect prudent leaders to prepare for the worst. After all, the pessimists have recently been vindicated by events. But that’s apparently too painful to think about. In normal times, leaders like to focus on the short term at the expense of the long term. But now the short term is really confusing, so leaders take refuge in projects that are years or decades away.

The president of the United States has decided to address this crisis while simultaneously tackling the four most complicated problems facing the nation: health care, energy, immigration and education. Why he has not also decided to spend his evenings mastering quantum mechanics and discovering the origins of consciousness is beyond me.

The results of this overload are evident on Capitol Hill. The banking plan is incomplete, and there is zero political will to pay for it. The president’s budget is being nibbled to death. The revenue ideas are dying one by one, while the spending ideas expand. By the latest estimate, the health care approach will cost $1.5 trillion over 10 years and the national debt will at least double, while the Chinese publicly complain about picking up the tab.

Anatole Kaletsky: Are democracy and capitalism incompatible?

What has happened – not only in America but also in Britain – to this promise of a calm, pragmatic response to the world’s economic problems? This week Mr Obama expressed outrage at the $165 million bonuses paid by AIG, the stricken insurance group, to executives in its financial products division who are responsible for most of its tens of billions of dollars in losses.

In Britain the row over Sir Fred Goodwin’s pension continues to grow. And in both countries, hatred of bankers is making it difficult for governments to take further action to stabilise the banks and support economic growth.

The behaviour of the bankers who first blew up the world financial system and then proceeded to loot it, is genuinely outrageous and deserves political retribution. But that should take the form of recovering the booty by the normal processes of law.

Obama's Approval Rating Slips Amid Division Over Economic Proposals

President Barack Obama’s approval rating has slipped, as a growing number of Americans see him listening more to his party’s liberals than to its moderates and many voice opposition to some of his key economic proposals. Obama’s job approval rating has slipped from 64% in February to 59% currently, while disapproval has jumped from 17% to 26% over this period.

Although most people think the new president is doing as much as he can to fix the economy and relatively few say Obama’s policies have made the economy worse, the public expresses mixed views of his many major proposals to fix the economy.

Notable and Quotable

Let’s just say in September, when Lehman failed, it took people two plus weeks to find out where all of the counterparties were. I am certain during that time, which is the same week that AIG came under significant duress, they thought the same thing. It would take a significant amount of time to name the counterparties.

Now, you know, several month later, they can know who the counterparties were, but at that time they didn’t know who the counterparties were, and that is what is so frightening about how perverted the system had gotten, in terms of people didn’t know where the bodies were. And so in a way, it was a Band-Aid approach to say, OK, here is money, get it where it needs to go, it buys them time.

And the government reaction in all of this seems to have been, OK, we need more time, we need more time.

The curious thing about Geithner rushing to get a plan was, they weren’t ready. You know, do your homework and then come to the table and have a real plan. But all of this, had all these unintended consequences, and so we are talking about a $165 million bonus pool when it is not the real issue.

Thomas Friedman: Obama’s Real Test

Let me be specific: If you didn’t like reading about A.I.G. brokers getting millions in bonuses after their company ”” 80 percent of which is owned by U.S. taxpayers ”” racked up the biggest quarterly loss in the history of the Milky Way Galaxy, you’re really not going to like the bank bailout plan to be rolled out soon by the Obama team. That plan will begin by using up the $250 billion or so left in TARP funds to start removing the toxic assets from the banks. But ultimately, to get the scale of bank repair we need, it will likely require some $750 billion more.

The plan makes sense, and, if done right, it might even make profits for U.S. taxpayers. But in this climate of anger, it will take every bit of political capital in Barack Obama’s piggy bank ”” as well as Michelle’s, Sasha’s and Malia’s ”” to sell it to Congress and the public.

The job can’t be his alone. Everyone who has a stake in stabilizing and reforming the system is going to have to suck it up. And that starts with the brokers at A.I.G. who got the $165 million in bonuses. They need to voluntarily return them. Everyone today is taking a haircut of some kind or another, and A.I.G. brokers surely can be no exception. We do not want the U.S. government abrogating contracts ”” the rule of law is why everyone around the world wants to invest in our economy. But taxpayers should not sit quietly as bonuses are paid to people who were running an insurance scheme that would have made Bernie Madoff smile. The best way out is for the A.I.G. bankers to take one for the country and give up their bonuses.

I live in Montgomery County, Md. The schoolteachers here, who make on average $67,000 a year, recently voted to voluntarily give up their 5 percent pay raise that was contractually agreed to for next year, saving our school system $89 million ”” so programs and teachers would not have to be terminated. If public schoolteachers can take one for schoolchildren and fellow teachers, A.I.G. brokers can take one for the country.

Steven Pearlstein: Wall Street's Dangerous Refusal to Learn

You have to wonder what else has to go wrong, how much more wealth will need to be destroyed, before the people on Wall Street get the message that it’s no longer business as usual.

The latest outrage, of course, is over the $400 million in retention bonuses promised to those financial geniuses at AIG’s Financial Products unit last year, months before the insurance giant was essentially taken over by the government in a bailout that already has required an injection of $170 billion in taxpayer money.

The legal argument for honoring these ill-considered contracts is that a deal is a deal and that trying to abrogate them will only wind up costing the government even more in legal fees and punitive damages. But that doesn’t mean the government and its handpicked new management team at AIG were powerless to renegotiate those contracts long before last weekend’s deadline.

David Leonardt: The Looting of America’s Coffers

Sixteen years ago, two economists published a research paper with a delightfully simple title: “Looting.”

The economists were George Akerlof, who would later win a Nobel Prize, and Paul Romer, the renowned expert on economic growth. In the paper, they argued that several financial crises in the 1980s, like the Texas real estate bust, had been the result of private investors taking advantage of the government. The investors had borrowed huge amounts of money, made big profits when times were good and then left the government holding the bag for their eventual (and predictable) losses.

In a word, the investors looted. Someone trying to make an honest profit, Professors Akerlof and Romer said, would have operated in a completely different manner. The investors displayed a “total disregard for even the most basic principles of lending,” failing to verify standard information about their borrowers or, in some cases, even to ask for that information.

The investors “acted as if future losses were somebody else’s problem,” the economists wrote. “They were right.”

David P. Gushee: Mr. President, we need more than lip service

But this kind of calculation is precisely what has gotten Christian political activists in trouble in the past, not just for 40 years but for 1,600 years. We gain access to Caesar in order to affect policy; we hold onto access even if it involves compromising some of what we want in policy; in the end, we can easily forget what policies we were after in the first place. I think this definitely happened to the Christian right. It doesn’t need to be repeated by the Christian center or left.

My understanding of the majestic God-given sacredness of human life tells me that a society that legally permits abortion on demand is deeply corrupt. It pays for adult sexual liberties with the lives of defenseless developing children. That practice, in turn, desensitizes society to the implications of paying for prospective medical cures with defenseless frozen embryos, which themselves are available because our society pays for medically assisted reproductive technology by producing hundreds of thousands of these embryos as spares. And yes, that same commitment to life’s sacredness has grounded my opposition to paying for national security with torture, or paying for today’s affluence with tomorrow’s environmental destruction.

Christian conscience requires me to make this case even if it has no chance of prevailing in American society. And if we lose on abortion, as it appears we will lose for a long time to come, Christian conscience requires me to ask the government not to require citizens to pay for procuring services that violate their sacred beliefs.

NY Times Week in Review: Has the Economy Hit Bottom Yet?

Which leads to a question: When we do hit the bottom ”” this year or years from now ”” how will we know?

There’s no easy answer.

Mr. Galbraith was not the first or last economist to acknowledge fallibility at predicting turning points. (Just think back to assurances by top government officials in early 2007 that the growing problems with subprime mortgages were “contained.”)

Forecasting the end of the current recession is even more difficult because it will hinge on how quickly and efficiently governments resolve the crisis in the banking system. Many investors continue to worry that the world’s biggest financial institutions are insolvent, despite assurances from Washington that those firms have plenty of capital.

How political leaders diagnose and fix the banks will be critical. Analysts say misguided and erratic government responses exacerbated Japan’s “lost decade” in the 1990s and the Depression of the 1930s. “The things that can screw it up are bad policies,” said Thomas F. Cooley, dean of the Stern School of Business at New York University.

Peter Steinfels: In Stem Cell Debate, Moral Suasion Comes Up Short

Almost no one was surprised this week when President Obama lifted restrictions on stem cell research that involved the destruction of human embryos. Even jaded Washington watchers are adjusting to the idea that this is a president with an eerie determination to do exactly what he said he would do during his campaign.

Those who approve such research applauded Mr. Obama’s action. (“Fantastic,” said one stem cell scientist on PBS.) Those who disapprove condemned it. (“Deadly,” said an anti-abortion leader in The New York Times.) But some commentary focused at least as much on the nature of the president’s moral argument as on the specific conclusions he reached.

When it comes to the controversy over human embryonic stem cell research, moral argument has not been much in evidence. The president spoke of a popular consensus in favor of it reached “after much discussion, debate and reflection.” That is a kindly description of the hype, exaggeration and denunciation that have dominated the controversy.